How Luxury Home Escrow Actually Works on the Eastside: A Step-by-Step Timeline

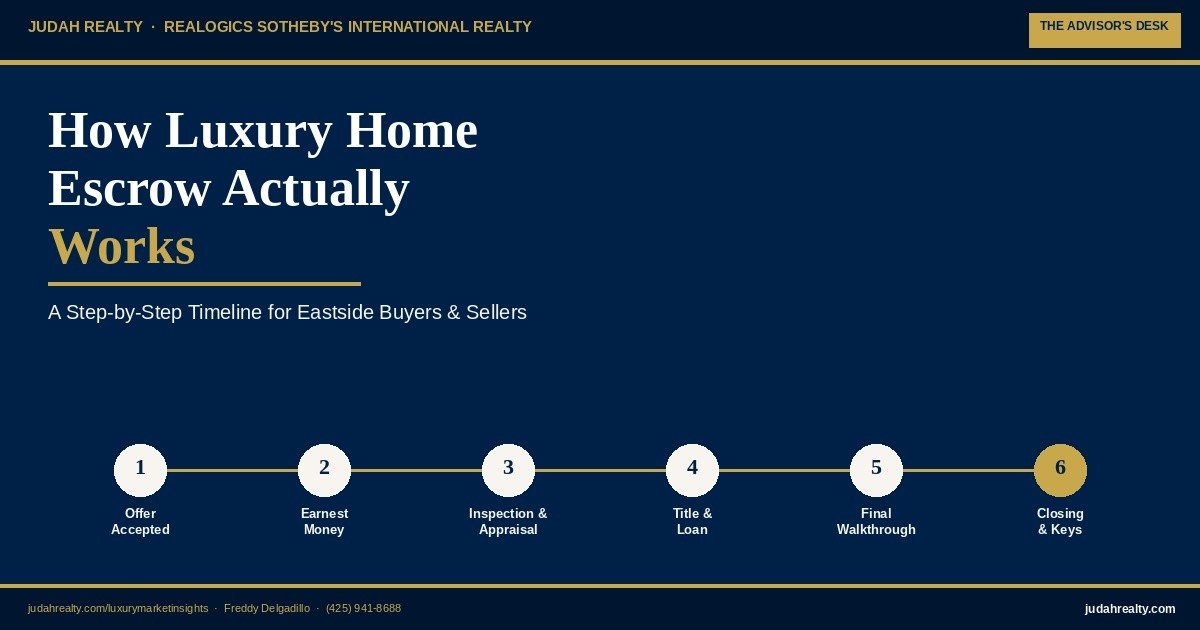

Escrow on an Eastside luxury home typically takes 30 to 45 days from accepted offer to closing. During that window, six key steps occur: earnest money deposit, inspection and appraisal, loan underwriting and title work, contingency removal, final walkthrough, and closing day funding and recording. This guide breaks down what happens at each step — and what to watch for.

You've found the right home. Your offer was accepted. And now comes the part of the process that feels the most opaque: escrow. For many buyers and sellers — even experienced ones — the weeks between an accepted offer and the day you get the keys (or hand them over) can feel like a black box. Things are happening. Documents are being signed. Deadlines are passing. But what, exactly, is going on?

This guide walks through the entire escrow process, step by step, using the timeline that applies to most Eastside luxury transactions. Whether you're a buyer wondering what to expect next, or a seller trying to understand why your closing date keeps getting referenced in emails from three different people, this is the explanation nobody gave you — until now.

The Escrow Timeline:

Six Steps, 30–45 Days

Here is the full journey at a glance. Each step is explored in detail below.

Offer Accepted — Escrow Opens

Day 0–2The moment the seller signs the accepted offer, the purchase and sale agreement becomes a binding contract — and "escrow" officially opens. The agreement is sent to an escrow company (a neutral third party that holds funds and documents until all conditions are met), and a closing date is established, typically 30 to 45 days out. Both the buyer's and seller's agents begin coordinating with the escrow officer, title company, and — if financing is involved — the lender.

At this stage, the contract specifies several important dates that will govern the rest of the process: the earnest money deadline, the inspection contingency deadline, the financing contingency deadline, and the closing date itself. These dates are not arbitrary — missing one can have real consequences for either party.

Freddy's Note: The first 48 hours after acceptance are when the most important calendar gets set. I review every date in the contract with my clients immediately — not the week before something is due. Knowing your deadlines on day one removes 90% of the stress that builds up later.

Earnest Money Deposit

Day 1–3Within a few days of acceptance, the buyer wires earnest money to the escrow company. This deposit demonstrates the buyer's serious intent and will be applied toward the purchase price at closing. For Eastside luxury homes, earnest money typically runs 1% to 3% of the purchase price — on a $3,000,000 home, that's $30,000 to $90,000.

This deposit is held in a secure escrow account — it does not go to the seller at this stage. It remains in escrow until closing, at which point it is credited toward the buyer's total funds due. If the transaction falls through for a reason covered by a contingency (such as a failed inspection within the inspection period), the earnest money is typically returned to the buyer. If the buyer backs out for a reason not covered by a contingency, the seller may be entitled to retain the earnest money as compensation.

Freddy's Note: Wire fraud targeting earnest money deposits is a real and growing risk. Never wire funds based on emailed instructions alone — always verbally confirm wire instructions directly with your escrow officer using a phone number you already have on file, not one provided in the email itself.

Inspection & Appraisal

Day 3–17This is the most active period of escrow for the buyer. A licensed home inspector conducts a thorough inspection of the property — structure, systems, roof, and (for waterfront properties) often a separate dock and bulkhead assessment. In Washington, the inspection contingency period is commonly 10 to 17 days from acceptance, though this is negotiable and specified in the contract.

Simultaneously, if the buyer is financing the purchase, the lender orders an appraisal — an independent assessment of the home's value to confirm it supports the loan amount. The appraisal is ordered early because appraisers are often booked out, and a delayed appraisal is one of the most common causes of closing date extensions.

If the inspection reveals issues, the buyer and seller negotiate: repairs, credits toward closing costs, or a price adjustment. Most inspection issues are resolved through negotiation rather than derailing the transaction — but the negotiation itself can take several days and is often the most tense part of escrow for both sides.

Freddy's Note: I always recommend scheduling the inspection within 48 hours of acceptance — not waiting until day 10 of a 14-day period. This gives you time to negotiate repairs or credits without feeling rushed, and it gives the seller's side adequate time to respond thoughtfully rather than under pressure.

Title Work & Loan Underwriting

Day 7–28While the buyer is completing inspections, two parallel processes are running in the background. First, the title company conducts a title search — reviewing public records to confirm the seller has clear ownership and identifying any liens, easements, or encumbrances that need to be resolved before closing. For waterfront properties, this also confirms shoreline easements and any recorded riparian rights.

Second, if the buyer is financing, the loan moves through underwriting — the lender's formal review of the buyer's financial documentation, the appraisal, and the title report. Underwriting is where "conditional approval" becomes "clear to close." This stage often produces additional document requests from the lender — bank statements, explanation letters, updated pay stubs — which can feel repetitive but are standard.

By the end of this period, all major contingencies — inspection, financing, and appraisal — are typically removed (formally waived in writing), meaning both parties are now contractually committed to closing, barring a major unresolved issue.

Freddy's Note: Respond to lender document requests within 24 hours, even if the request seems redundant. Underwriting delays are one of the most common reasons closings get pushed back — and they are almost always on the buyer's side of the process, not the lender being slow.

Final Walkthrough

Day 28–30One to two days before closing, the buyer (often with their agent) conducts a final walkthrough of the property. This is not a second inspection — it is a confirmation that the property is in the same condition as when the offer was accepted, that any agreed-upon repairs have been completed, and that the home is being left in the condition specified in the contract (including which fixtures, appliances, or other items convey with the sale).

If something is wrong at the final walkthrough — a repair wasn't completed, or something is missing or damaged — this is the last opportunity to address it before funds are released at closing. Resolution at this stage typically involves a holdback of funds in escrow until the issue is corrected, rather than delaying the entire closing.

Freddy's Note: Schedule the final walkthrough as close to closing as logistically possible — ideally the morning of or the day before. A walkthrough done four or five days early loses its purpose; a lot can happen to a property in that window, including a final round of moving damage from the seller's move-out.

Closing Day — Funding & Recording

Day 30–45Closing day involves several coordinated steps. The buyer typically signs final loan documents one to two days before the closing date — this is sometimes called "signing" as distinct from "closing." On the actual closing date, the lender wires the loan funds to escrow, and the buyer wires their down payment and closing costs (the earnest money from Step 2 is credited at this point).

Once escrow confirms all funds have been received, the deed is recorded with King County (or the applicable county), which officially transfers title to the buyer. Recording typically happens by early afternoon. Once recording is confirmed, the transaction has "closed" — the buyer can take possession (get the keys), and the seller's proceeds are wired out, usually the same day or the following business day.

For sellers, this is also the day prorated property taxes, HOA dues, and any other shared costs are settled through the closing statement — the final accounting of who owes what to whom.

Freddy's Note: Recording times vary by county and can occasionally be delayed until the next business day if closing happens late in the afternoon or on a Friday. I always build in a buffer when scheduling move-out and move-in logistics — never plan a moving truck for the exact closing date with no flexibility.

What Can Go Wrong:

And How Each Issue Is Typically Resolved

Most escrows close on time and without drama. But understanding what can cause delays — and how those situations are normally resolved — removes a significant amount of anxiety from the process.

Appraisal Comes in Below Purchase Price

If the appraisal value is lower than the agreed purchase price, the buyer's loan amount may be affected, since lenders base loan amounts on the lower of purchase price or appraised value. Resolution options include the buyer making up the difference in cash, the seller reducing the price to match the appraisal, a negotiated middle ground, or — in rare cases — the buyer challenging the appraisal with additional comparable sales data. In a market with rising inventory, like the Eastside is currently experiencing per the May 2026 NWMLS data, appraisal gaps can become slightly more common as comparable sales data lags behind asking prices.

Title Issue Discovered

Occasionally a title search reveals an unresolved lien, an old easement, or a recording error. Most title issues are resolved by the seller before closing — paying off an old lien, for example — and title companies are experienced at clearing these efficiently. Significant title issues are rare but can extend the closing timeline by days or, occasionally, weeks.

Financing Delay

If underwriting takes longer than expected — often due to a document request that wasn't fulfilled quickly — the closing date may need to be extended by a few days. This is typically handled through a mutually signed addendum extending the closing date, and is one of the most common (and most manageable) delays in the process.

Repair Disputes After Inspection

When buyer and seller disagree on the scope or cost of repairs identified during inspection, negotiation can extend over several days. Most resolutions involve a credit at closing rather than the seller completing repairs themselves — this is often faster and avoids disputes over repair quality.

For sellers currently evaluating whether to list, understanding this timeline matters for planning — especially in a market where, as covered in the seller advisory guide published earlier this month, different Eastside submarkets are moving at different speeds. And for waterfront buyers specifically, the hidden costs guide covers the additional due diligence items — dock and bulkhead inspections, permit history — that often run in parallel with the standard escrow timeline above.

Frequently Asked Questions:

Luxury Home Escrow on the Eastside

How long does escrow take on a luxury home in Washington state?

Escrow on a luxury home in Washington state typically takes 30 to 45 days from accepted offer to closing, though it can extend to 60 days or more for properties with complex financing, waterfront due diligence, or 1031 exchange requirements. Cash transactions can close in as little as 14 to 21 days. The exact timeline depends on the financing contingency period, inspection period, title work, and any negotiated repair periods.

What is earnest money and how much is typical for a luxury home purchase?

Earnest money is a deposit a buyer provides to demonstrate serious intent to purchase, held by the escrow company and applied toward the purchase price at closing. For luxury homes on the Eastside, earnest money typically ranges from 1% to 3% of the purchase price — for a $3,000,000 home, that is $30,000 to $90,000. The amount is negotiable and specified in the purchase and sale agreement.

What happens if a home inspection reveals problems during escrow?

If a home inspection reveals issues, the buyer typically has a defined inspection contingency period (commonly 10 to 17 days in Washington) to review the report and respond. The buyer can request repairs, request a price reduction or credit toward closing costs, or in some cases withdraw from the contract with earnest money returned, depending on the contingency terms. Most inspection issues are resolved through credits or repair agreements rather than derailing the transaction.

What is title insurance and why is it required?

Title insurance protects the buyer and lender against claims or defects in the property's title not discovered during the title search — such as undisclosed liens, ownership disputes, or recording errors. Washington escrow includes a title search and issuance of a title insurance policy as standard practice. For waterfront properties, title work also confirms easements, riparian rights, and shoreline access agreements recorded against the property.

What happens on closing day for a luxury home purchase?

On closing day, the buyer's funds and the lender's loan funds are transferred to escrow, the deed is recorded with the county, and title officially transfers to the buyer. The buyer typically signs final loan documents 1-2 days before closing and receives keys once the deed has recorded — usually by early afternoon on the closing date. Sellers receive proceeds via wire transfer, typically the same day or the following business day.

Freddy Delgadillo

Luxury Real Estate Advisor · Realogics Sotheby's International Realty

For Buyers

Going Under Contract Soon? Let's Walk Through Your Timeline Together.

Every escrow has its own rhythm — financing type, inspection scope, and title nuances all shape the timeline. Before you go under contract on your next Eastside home, let's map out exactly what your specific transaction will look like, step by step, so nothing catches you off guard.

For Sellers

A Smooth Escrow Starts Before You List.

The sellers who experience the fewest surprises during escrow are the ones who prepared for it before listing — clean title, organized disclosures, and realistic expectations about timing. If you're considering listing your Eastside home, let's talk about how to set up your transaction for a smooth close from day one.

ABR® · Accredited Buyer's Representative | CRS · Certified Residential Specialist | GRI · Graduate REALTOR® Institute | CLHMS · Certified Luxury Home Marketing Specialist