What Happens If Your Luxury Home Appraisal Comes in Low? A Buyer's and Seller's Guide

When an appraisal comes in below the contract price, the NWMLS Financing Addendum sets a defined timeline: the buyer has 3 days to deliver a formal Notice of Low Appraisal, the seller then has 10 days to respond with one of four options, and the buyer has a final 3 days to accept, waive the financing contingency, or terminate. Formally challenging an appraisal after it's finalized rarely succeeds — the more effective approach is providing the appraiser with comparable sales data and a documented upgrade list before the report is completed.

You're a few weeks into escrow. Inspection went fine. Financing is moving along. Then your lender calls: the appraisal came in below the contract price. For a moment, it feels like the entire deal might be at risk.

Here's the reality, based on what I've actually seen happen on the Eastside: in the past four years, I've had exactly two transactions where the appraisal came in low — and in both cases, the deal closed. Low appraisals are far less common on the Eastside than buyers fear, and when they do happen, there is almost always a path forward. This guide walks through exactly what happens, what your real options are, and the specific tactic I use to prevent low appraisals before they happen.

What an Appraisal Actually Is

(And Why It Exists)

An appraisal is an independent, professional opinion of a property's market value, conducted by a licensed appraiser on behalf of the lender. Lenders require it because they are extending a loan secured by the property — they need confirmation that the home is actually worth what they're lending against, separate from what the buyer and seller agreed to pay.

The appraiser visits the property, evaluates its condition, size, and features, and compares it to recently closed sales of similar homes in the area — known as "comparable sales" or "comps." The appraised value is the appraiser's professional conclusion based on that analysis. It is not the same as the contract price, and the two numbers are not always identical.

On the Eastside specifically, appraisals are fairly reliable at the price points I work in. Most come in at value or within 2–3% of the contract price. Significant gaps are uncommon — but they do happen, and understanding the process removes most of the anxiety when they do.

A professional appraisal in progress at a luxury Eastside home

The Formal Process:

What the NWMLS Contract Actually Says

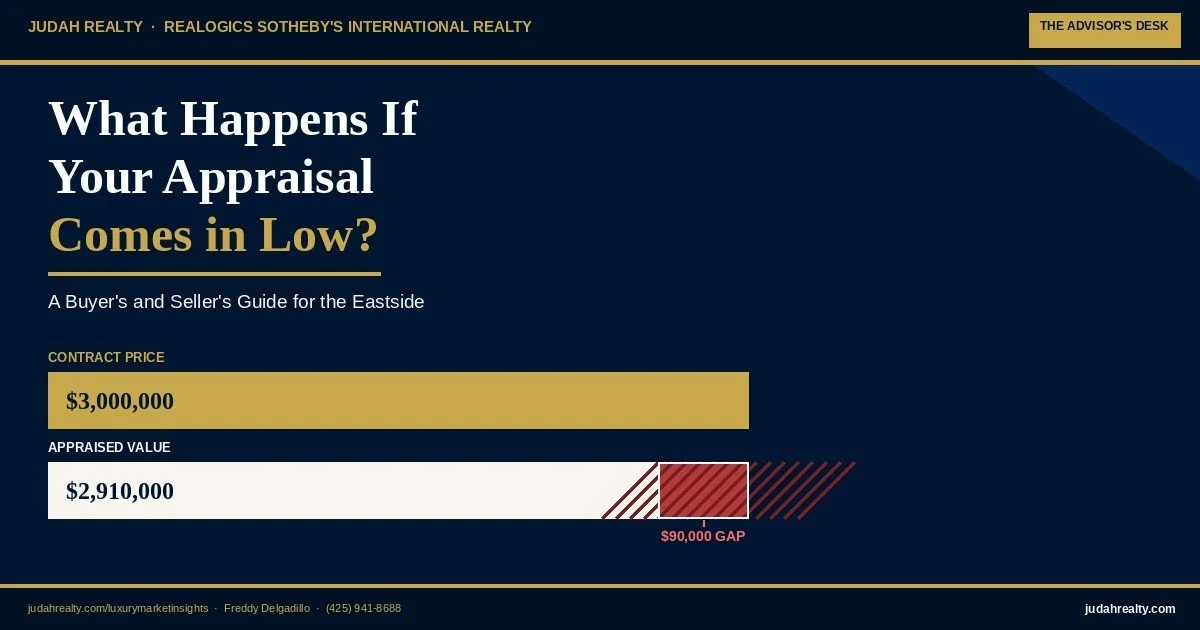

Here's the important context: lenders base loan amounts on the lower of the appraised value or the contract price — not the contract price alone. If your home is under contract for $3,000,000 and the appraisal comes back at $2,910,000, the lender will only finance based on $2,910,000. That $90,000 gap has to be resolved — and on the Eastside, that resolution follows a specific, defined procedure written directly into the Financing Addendum (NWMLS Form 22A) attached to nearly every financed purchase and sale agreement.

This isn't an informal negotiation with no structure. It's a sequence of notices and response windows, each with its own deadline. Here's exactly how it works.

Step 1: Buyer's Notice of Low Appraisal

3 DaysIf the lender's appraised value comes in below the purchase price, the buyer has 3 days after receiving a copy of the appraisal to deliver a formal "Notice of Low Appraisal," which must include a copy of the appraisal itself. This is a contractual deadline — if the buyer doesn't act within this window, the right to invoke this process can lapse.

Step 2: Seller's Response

10 DaysOnce the seller receives the buyer's notice, the seller has 10 days to choose one of four specific responses written into the contract: (1) request a reappraisal or reconsideration of value at the seller's own expense; (2) consent to reduce the purchase price to match the appraised value; (3) propose a reduced price that's still higher than the appraisal, with the buyer covering the remaining gap in cash; or (4) reject the buyer's notice of low appraisal outright. Each option carries different consequences for both sides, which is exactly why having an advisor walk through this decision with you matters.

Step 3: Buyer's Reply

3 DaysAfter the seller responds (or after the seller's 10-day window expires without a response), the buyer has 3 days to act. If the seller rejected the notice or didn't respond, the buyer must either waive the financing contingency and proceed at the original price, or terminate the agreement with earnest money refunded. If the seller proposed a reduced price with the buyer covering part of the gap, the buyer has 3 days to accept that arrangement or terminate. Critically: if the buyer does nothing during this reply window, the agreement automatically terminates and earnest money is refunded to the buyer — inaction is not a neutral outcome, it's a default termination.

A Real Example: The Issaquah Duplex

One of the two low appraisals I've encountered in the past four years was on an Issaquah duplex listing. The appraisal came in below the contract price, and we followed this exact process — buyer's notice, seller's response, buyer's reply. Rather than asking my sellers to reduce the price, the seller proposed the reduced-price-with-buyer-gap option, and the buyer accepted, covering the shortfall in cash to keep the deal moving at the agreed price. The transaction closed on schedule, my sellers received their full agreed price, and the buyer secured the property they wanted. Understanding the formal timeline in advance is what kept this moving smoothly instead of becoming a source of panic for either side.

Can You Challenge

a Low Appraisal?

Within the formal process above, there is one path built directly into the contract: the seller can request a reappraisal or reconsideration of value, at the seller's own expense, by the same appraiser or another appraiser acceptable to the lender. The catch, per the contract language, is that the lender may decline to accept a reappraisal or reconsideration of value — so this option carries real cost and no guarantee of success. In my experience, once an appraisal report is finalized, getting the number changed through this formal channel succeeds less often than buyers and sellers hope.

The far more effective approach is preventing the low appraisal in the first place, by giving the appraiser the right information before the report is completed — not trying to dispute it after the fact.

My Approach: Educate the Appraiser at the Property

When comparable sales are limited or a neighborhood has unique characteristics that don't show up in a standard data pull, I make a point of being present — or having my team present — during the appraisal visit. The goal is straightforward: give the appraiser context they wouldn't otherwise have access to.

This typically includes two things. First, neighborhood-specific value drivers — explaining how one community on the Eastside differs from another nearby area that might look similar on paper but commands different pricing due to school assignment, lot characteristics, or proximity to amenities. Second, and most importantly, a documented upgrade and finishes list — a written summary of renovations, premium finishes, and improvements that an appraiser may not otherwise notice or have a reference point for, since many MLS listings don't capture this level of detail.

This single document — an upgrade list with specifics rather than vague claims — is one of the most underused tools in luxury real estate. Appraisers are working with limited time and data. Giving them a clear, specific reference for what makes a property different from its nearest comparable sales helps them arrive at an accurate value the first time, rather than relying on the formal — and uncertain — reappraisal request after the fact.

What If You're

Paying Cash?

Cash buyers are in a fundamentally different position. Because there's no loan amount tied to the appraised value, a low appraisal doesn't affect a cash buyer's ability to close at the agreed price. Many cash buyers still order an appraisal for their own informational purposes, but it functions as due diligence rather than a financing requirement.

On the Eastside specifically, cash transactions have become less common over the past three years — most buyers I work with are financing, typically with substantial down payments in the 20–40% range. That financial cushion is precisely why most appraisal gaps get resolved by the buyer simply covering the difference: the cash reserves to do so are often already part of their financial picture.

What Sellers Can Do

Before Listing to Reduce Appraisal Risk

If you're preparing to sell, there are concrete steps that reduce the likelihood of an appraisal gap creating friction in your transaction.

Price Based on Closed Comps, Not Aspiration

The further your listing price drifts from recently closed comparable sales, the higher your appraisal risk. This doesn't mean underpricing your home — it means understanding where genuine market value sits before setting your number, which is exactly the kind of analysis covered in the seller advisory guide published earlier this month.

Prepare an Upgrade and Finishes Document

Before listing, document every significant upgrade, renovation, and premium finish in your home — kitchen remodels, smart home systems, premium flooring, landscaping investments, mechanical system replacements. This document becomes invaluable if an appraisal is ever borderline, giving your advisor something concrete to share with the appraiser rather than relying on the appraiser noticing these details independently.

Be Available During the Appraisal Visit

Having a knowledgeable representative present during the appraisal — someone who can speak to neighborhood value drivers and walk through the upgrade list in person — is one of the most effective preventive steps available. This is standard practice I follow on every listing where comparable sales data is limited or where the property has unique value drivers a quick data pull won't surface.

Why This Matters More

in the Current Eastside Market

As covered in the May 2026 NWMLS Market Update, Eastside inventory is rising and the market is shifting toward more balance. In this environment, appraisal gaps become slightly more relevant for one specific reason: appraisers rely on closed sales data, which by definition lags behind a fast-moving or rapidly adjusting market.

In submarkets where pricing has moved quickly — either up during a hot stretch or down as inventory rises — the most recent closed comps an appraiser can access may not fully reflect current conditions. This doesn't mean appraisal gaps are becoming common across the board; most Eastside appraisals remain accurate within a tight range. But it does mean the preventive steps outlined above — accurate pricing, a documented upgrade list, and an informed presence during the appraisal — matter more now than they did when the market was moving in one consistent direction.

For buyers specifically navigating waterfront purchases, appraisal considerations often intersect with the additional due diligence covered in the hidden costs of waterfront ownership guide — particularly since waterfront comparable sales are inherently more limited than standard residential comps, making the upgrade-list strategy described above even more valuable.

Frequently Asked Questions:

Luxury Home Appraisals on the Eastside

What happens if a home appraisal comes in below the contract price?

On the NWMLS Financing Addendum (Form 22A), a low appraisal triggers a specific contractual timeline: the buyer has 3 days after receiving the appraisal to deliver a formal Notice of Low Appraisal. The seller then has 10 days to respond with one of four options — request a reappraisal at the seller's expense, consent to reduce the price to the appraised value, propose a reduced price with the buyer covering part of the gap, or reject the notice. The buyer then has 3 days to accept, waive the financing contingency, or terminate with earnest money refunded.

Can you challenge or appeal a low home appraisal?

Within the formal contract process, the seller can request a reappraisal or reconsideration of value at the seller's own expense, using the same or another lender-acceptable appraiser. However, the lender may decline to accept the new value, so this path carries cost without a guaranteed outcome. The more effective approach is providing the appraiser with comparable sales data and a documented upgrade list before the original report is finalized.

What happens if the buyer doesn't respond after a low appraisal?

If the buyer takes no action during their 3-day reply window after the seller's response (or after the seller's 10-day window expires without a response), the agreement automatically terminates and the earnest money is refunded to the buyer. Under the NWMLS contract, inaction during this period is not a neutral holding pattern — it results in a default termination, which is why tracking these deadlines closely matters for both sides.

How often do luxury home appraisals come in low on the Eastside?

On the Eastside, appraisals coming in significantly below contract price is relatively rare — most appraisals land at or within 2-3% of the agreed purchase price. However, in submarkets where pricing has moved quickly relative to recent comparable sales, low appraisals become more frequent, since appraisers rely on closed sales data that can lag behind a fast-moving market.

Do cash buyers need to worry about appraisals?

Cash buyers typically still order an appraisal for their own due diligence, but they are not bound by a lender's appraisal contingency, since there is no loan amount tied to the appraised value. This means a low appraisal does not affect a cash buyer's ability to close at the agreed price, though it may still be a useful negotiating data point if discovered during the transaction.

What can sellers do to prevent a low appraisal before listing?

Sellers can reduce appraisal risk by pricing in line with recent closed comparable sales rather than aspirational pricing, preparing a detailed list of property upgrades, renovations, and finishes for the appraiser's reference, and working with an advisor who provides supporting market data directly to the appraiser at the time of the appraisal visit. Being present, or having a knowledgeable representative present, during the appraisal to share this information is one of the most effective preventive steps.

Freddy Delgadillo

Luxury Real Estate Advisor · Realogics Sotheby's International Realty

For Buyers

Know Your Options Before You're In the Middle of One.

Most buyers never think about appraisal risk until a lender calls with unexpected news. Before you write an offer on your next Eastside home, let's talk about your specific price point, your down payment cushion, and exactly what your options would be if this came up — so nothing about the process surprises you.

For Sellers

The Right Pricing Strategy Prevents This Conversation Entirely.

An accurate, well-documented listing — priced against real comps with a complete upgrade history ready for the appraiser — is the single best protection against appraisal surprises. If you're preparing to list your Eastside home, let's build that foundation before you go to market.

ABR® · Accredited Buyer's Representative | CRS · Certified Residential Specialist | GRI · Graduate REALTOR® Institute | CLHMS · Certified Luxury Home Marketing Specialist